Blog

Three pros and cons of pound-cost averaging

It has been a volatile few years for financial markets, firstly the Covid-19 pandemic caused a multinational global shut down and now the war in Ukraine, which is again causing more global pressures. Here’s how investors could mitigate the challenge of today’s bumpy markets by investing on a regular basis.

Inflation has been a significant factor in battering economies around the world, with prices rising, people are spending less, causing a reduction in economic growth. Unfortunately, it is very difficult for the average investor to take advantage of such volatility, as with imperfect knowledge and limited time, it can prove difficult to make informed decisions. What an investor can do however is try to take advantage of pound-cost averaging.

Essentially, pound-cost averaging involves purchasing investments on a regular basis to take advantage of troughs in the market. Pound-cost averaging might sound complicated, but it simply means investing into the market at regular intervals, also known as ‘drip-feeding’.

When you decide to invest, you can either invest all at once and hope that the market performs consistently well so your investment increases month-on-month, or you can drip feed that lump sum into your investment pot with regular payments over the course of a few weeks, months or years.

The idea of pound-cost averaging is to make regular contributions instead of a lump sum to try and smooth out the ups and downs of the market. This method can reduce the risk – and pain – of buying just before the market drops.

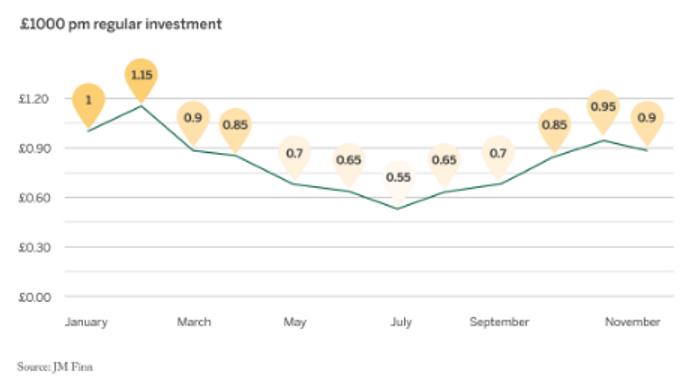

In the example below, an investor has invested £1,000 each month for a year, investing in the prices marked. The average price held by the investor having completed the investment timeframe is £0.7869, having invested at every point on this chart.

Clearly, the investor has taken advantage of the dips and has obtained a price which is currently below the current share price of £0.90. On the £12,000 invested, the investor is profiting circa 14% (£1,724) from the units and average price they hold.

Comparatively, if they had invested the lump sum of £12,000 in January, they would currently be losing 10% (£1,200), with the portfolio value being £10,800.

Benefits of pound-cost averaging

1) Discipline in volatile times

When the stock market turns from upturn to downturn, it is usually a very stressful time for investors and can cause irrational and erratic behaviour. Investors may make hasty decisions, such as making lump sum withdrawals or investments to try and catch “the dip”.

If these strategies do not work, the situation can become very difficult, especially for those who perhaps can’t afford the losses from the decisions made. Having pound-cost averaging as a strategy in place means regular investments, without the issue of needing to make decisions. Investors will be disciplined in that they will not invest on their emotions, as investments will be made automatically.

2) Smoothed returns

As the stock market rises and falls, pound-cost averaging will purchase at differing prices and will smooth out returns. This is because investments made are at both highs and lows, therefore the average could be somewhere in-between the high and low price range.

3) Planned investments

The regular investments will be made out of surplus affordable income, therefore the investments should not impact an investor’s lifestyle if there were to be a downturn, limiting the emotional stress of the stock market.

Drawbacks of pound-cost averaging

1) The impact of inflation

Pound-cost averaging requires a regular investment of cash. Over time cash that is held un-invested can have its value eroded by inflation, as the cash balances are not benefiting from the potential growth of the stock market.

2) Purchasing when the market is rising

Pound-cost averaging works both ways in that it will purchase highs and lows of the market, therefore it is not so beneficial if the regular investments are purchasing at perceived markets highs, which will cause the average price held on an account to increase.

In a rising market, you end up buying shares at increasing prices. In this case, investing a lump sum from the start of a rising market would mean you bought all your shares at the lower price, which could potentially mean a higher return.

3) Potentially increased costs

An investor should check and compare the costs of investing regularly rather than investing a lump sum. It could be that investing regularly may prove more expensive, dependent on the type of investment selected.

Michael Law is a paraplanner at JM Finn