Blog

Vanguard lifts the lid: The truth about ‘pound cost averaging’

Should you invest a lump sum of money straight away or drip-feed it into the market? The historical evidence is clear for investors to see…

If ever you have the good fortune to receive a windfall due to an inheritance, bonus payment or property/business sale, you will know that one of the big questions is how to invest the cash.

Should you invest all of it at once or should you ‘pound-cost-average’ by breaking the lump sum into smaller chunks and investing them over a longer period of time?

It’s a dilemma that should not be confused with regular saving, which is when a pre-defined amount of money leaves your bank account each month and purchases however-many fund units are possible at the fund’s prevailing price, so that your average fund-unit cost changes over time.

That’s unquestionably a positive form of ‘pound-cost averaging’ because by effectively outsourcing your investments to a pre-programmed financial transaction, you don’t have to worry about market timing and have a manageable and disciplined plan to help grow your wealth. Here, each individual monthly payment represents its own individual lump sum.

But what about when you’re presented with a large lump sum and you have the choice to invest in one go or to spread it out? What do you do then?

To work out which strategy would be best, we’ve compared the performance of cost averaging and lump sum investments across various markets, time periods and return assumptions. We also did it in a range of different currencies, including pounds.

The findings of our research team (Megan Finlay and Josef Zorn) are unequivocal: Lump-sum investment strategies tend to beat cost-averaging strategies about two-thirds of the time.

The historical evidence

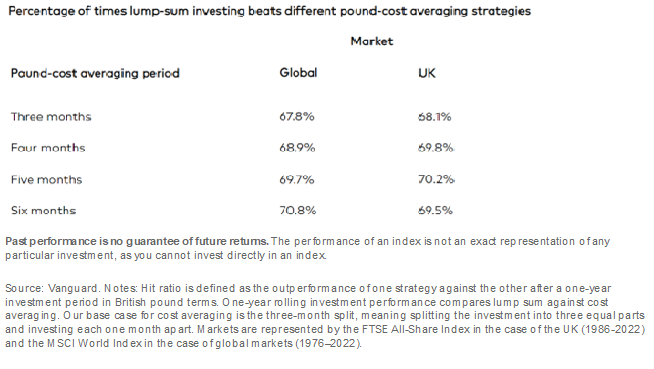

Using the MSCI World Index, our experts looked at the performance of global stock markets between 1976 and 2022 and contrasted the fortunes of a lump sum investment versus various pound-cost averaging investment strategies on a rolling one-year basis.

What they found, as the table below shows, is that the more spread out the investments and the less time a portfolio is fully invested, the higher the percentage win, or ‘hit ratio’, of a lump sum strategy.

So much so, that when an investment was split into six monthly payments, the win ratio for the lump sum strategy rose to almost 71%.

It’s a historical trend that’s discernible too when we look at just the UK stock market, as the table also shows.

In most cases, our researchers found that the less time fully invested, the less the potential to maximise investment returns.

In short, since lump-sum investing outperforms on average, you are usually better off investing immediately instead of holding back a portion of the potential investment.

What difference could it make in your wealth?

How might this observable difference in performance translate in monetary terms? The answer is it really depends on how markets perform in practice – on factors beyond an investor’s control – since markets can go down as well as up, which means you could potentially get back less than you invested.

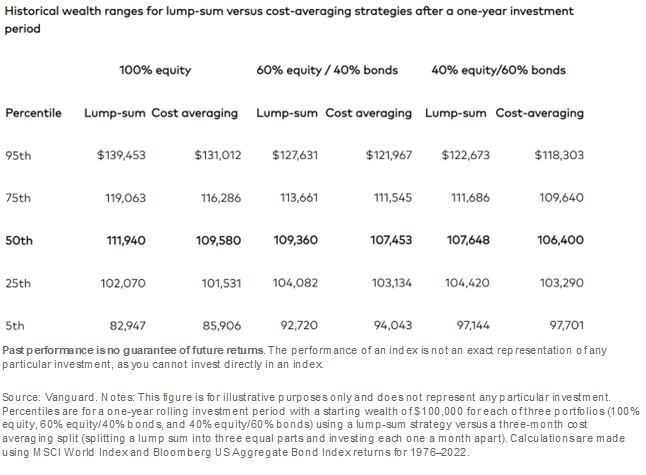

What we can say, nonetheless, is that in most cases, based on the historical evidence, investing a lump sum straight away is significantly more likely to grow your wealth than cost averaging. That’s illustrated by the chart below which shows how a portfolio might have grown over a one-year period at any point between 1976 and the end of 2022.

Although the data here is in US dollars (we start with a portfolio of $100,000), we would expect to see a similar pattern in pounds, given the ‘hit ratios’ shown earlier.

What can be observed is how in at least 75 out of every 100 scenarios measured during this period (10,000 different simulations were run in all), the lump-sum approach would have grown the investor’s portfolio by more than would have been the case if their investments had been spread over three months.

This remained true regardless of whether the money was invested in a 100% shares portfolio or in portfolios split 60/40 and 40/60 between shares and bonds.

What about after a one-year investment period?

It should be stressed that the performance data above excludes costs and is just for illustrative purposes. The observable trend, nonetheless, is clear.

So, when there’s a choice to be had, remember that lump sum investing holds a distinct edge over pound-cost averaging.

Still, as shown in the lowest 5th percentile of market performances during the study period – the bottom row of the table – lump sum investing can initially hurt your wealth more than cost averaging if you happen to be particularly unlucky with your timing and invest during a downturn.

It’s why, for more cautious and loss-averse investors, pound-cost averaging a lump sum rather than investing it all at once can still play a useful role by shielding you from the possibility of regret, even if it reduces your returns in the long run, as the evidence would suggest.

Investing a lump sum gradually is also better than not investing at all since pound-cost averaging has historically performed better than if you just stuck with cash (outperfmormed cash 69% of the time), our experts found.

James Norton is head of financial planners at Vanguard, Europe