Insurance

Homeowners warned over inadequate insurance cover for flooding as claim limits stall

Homeowners may be left out of pocket for claims relating to bad weather or flooding, as some policies cover just £15,000 for alternative accommodation which won’t last long given soaring rents.

In some parts of the country, rents have risen by 25% in a year, but insurance lags behind these soaring accommodation costs, according to financial information business, Defaqto.

Its research revealed that many insurance policies may not include enough cover for those who are forced out of their homes due to bad weather, particularly in light of the recent floods.

As well as having to repair and replace belongings, flood victims may also have to live elsewhere while the property is dried out.

A seriously flooded house can take up to a year or more to put right, while it’s not unheard of to be out of your home for as long as 18 months to two years.

But with a shortage of available builders and supplies, coupled with soaring accommodation costs, insurance policies may not provide enough cover.

Click here to view our Sponsored Content Hub

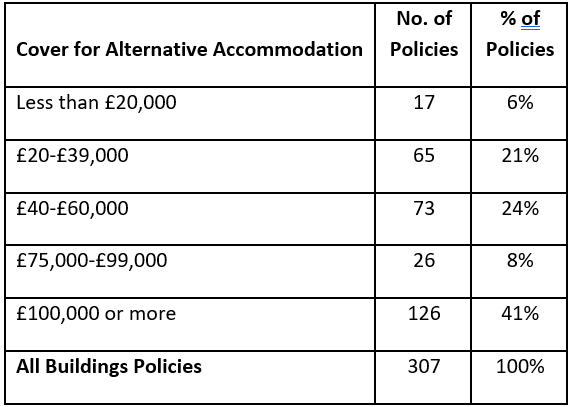

Some policies offer as little as £15,000 for alternative accommodation – equivalent of six months’ rent for a house in London – with almost one in four offering less than £40,000.

Defaqto said while this might sound a lot, in parts of the country this could easily be used up in an extended repair process. It also found a small number of policies even provide cover for less than six months of temporary accommodation.

Here are its findings on buildings insurance policy cover for alternative accommodation:

Source: Defaqto Matrix Database on 4 November 2022

Check your policy small print

Brian Brown, consumer finance expert at Defaqto, said: “While there are obvious things people can do to protect their homes against flood damage, including very carefully choosing the place to live, climate change is making a mockery of even those decisions as we experience flooding in areas which were previously thought to be safe.

“If you are unlucky enough to have your house damaged by storms and flooding, home buildings and contents insurance is intended to pay for any damage, provided you have cover. Buyers should beware of the insurance small print and check their cover. Many people underestimate just how much those costs might be and are caught out.

“Many policies have not increased their limits in line with the current rental market and homeowners could be caught out if they have to be out of their property for an extended period for repairs.”