Getting Started

Big investment trust discounts on well-known companies: Should you buy?

Investment trust discounts have widened again for both equities and alternative assets. But is this a buying signal too big to ignore or are they cheap for a reason?

Investment trusts are run by fund managers and offer pooled investments in companies which trade on the stock market. They allow investors to tap into a range of assets including shares, bonds and property. Investors can also access niche areas such as private equity and debt, as well as infrastructure.

They’ve been around for over 150 years, with one of the major advantages being their closed-ended, liquid structure meaning for every seller, there must be a buyer. This allows managers to own assets for the long term without having to sell them to meet redemptions when investors want their money back.

Just over six months ago, the Association of Investment Companies (AIC) noted that of the 38 sectors (excluding VCTs) with at least three companies listed, 37 were trading at a discount, averaging -14%.

But now, all 38 sectors spanning equities (23) and alternatives (15) are trading at an average discount.

And this discount has widened to an average -17.5%. The AIC says the last time discounts were persistently in double digits was during the financial crisis of 2008.

At the end of June 2023, the sector with the deepest discount continues to be North America (-28.5%), followed by Flexible Investment (-25.2%) and Global Smaller Companies (-17%).

Delving into individual companies, the AIC notes GRIT Investment Trust plc trades on a discount of -85.9%, Tetragon Financial Ord on -67.2% and Hansa Investment Company Ltd ‘A’ Class A at -41.7%.

At the other end of the scale, JPMorgan Emerg E, ME & Africa Sec Plc is trading at a premium of 107.95%.

Investment trust discounts: How do they arise?

A common measure of the underlying value of a share in an investment company is the net asset value (NAV) per share.

The NAV is the value of the investment company’s assets minus any liabilities it has.

The NAV per share is worked out by dividing the NAV by the number of shares in issue which is often different to the share price. And it is this difference that represents either a discount or premium.

The AIC explains that when a trust’s share price is lower than the underlying investments held by the trust (the NAV), the trust is trading on a discount to NAV and means the shares are cheap.

When investment trust shares are trading above the value of their assets, this is known as a premium to NAV and means the shares are expensive.

As an example, a 10% discount means, in theory, you are buying 100p of assets for 90p.

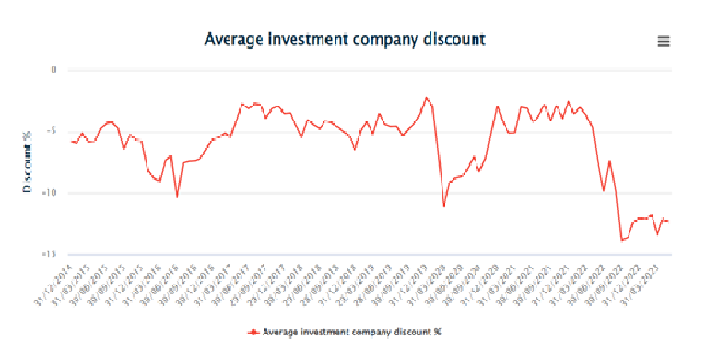

The graph below (source: AIC) shows the average investment company discount since 2014, revealing that the discounts have widened over time:

Does an investment trust discount signal a buying opportunity?

There are numerous reasons why discounts (and premiums) emerge, including market sentiment, sentiment towards a particular sector (for example, UK equities), recent performance of the investment company, or the success of an investment company’s marketing initiatives.

However, the AIC cautions that the current discount figures are based on the current share prices and the most recent reported NAVs available. For alternative assets, these NAVs may be several weeks or months out of date, because of the lag between NAV valuation points and when the NAVs are reported.

“In falling markets, recent discounts can appear unusually wide because of this lag in NAV reporting; when the new (lower) NAVs come out the historical discounts will appear narrower”, it explains.

However, the AIC adds: “We still believe current discounts are wider than the historical average, both for equities and alternative assets.”

Last year was difficult for markets because of the war in Ukraine, high inflation, and rising interest rates and these headwinds have continued into 2023

“Many investment company analysts think the wide discounts represent buying opportunities. In the past, brave investors who have bought investment companies when times are tough have profited in the long run”, it adds.

A discount can be attractive to investors as the return will get a boost if the discount narrows at the same time as underlying performance improves. But discounts can also widen “so a discount should never be your main reason for investing”, the AIC warns.

Is an investment cheap for a reason?

It’s important to look under the hood of the investment as sometimes it may be cheap for a reason. This could include poor short- or long-term performance, or specific circumstances affecting that investment company.

“You need to understand the reason for the discount before you invest,” the AIC warns.

It suggests investors compare an investment company’s current discount to the average discount of investment companies in its sector, as well as its own history before coming to a conclusion about whether a discount represents an opportunity or not. Data can be found on the AIC website.

“Investors should also be aware of any discount control policies that the investment company may have: for example, buying back its own shares to reduce a discount when the discount reaches a particular level (say, 10%). Discount control policies can help reduce discount volatility but they are not a panacea or a guarantee that the discount will never breach the targeted level,” it says.

The AIC adds: “While buying investment companies at discounts can be attractive, far more important than the discount is the underlying investment strategy, portfolio and performance. This is particularly true over the longer term, over which discounts often revert to the mean.

“Investors should be wary of the danger of obsessing over discounts and spend more time researching what the investment company invests in, what it is aiming to achieve, and whether that suits the investor’s own personal circumstances and needs.”

Three big/well-known investment trusts at a notable discount

Darius McDermott, managing director of FundCalibre and Chelsea Financial Services lists these three investment trusts offering big discounts and the reasons why investors could consider them in their portfolios:

1) Schroder British Opportunities

This trust is a pure play on the recovery of UK equities. It invests in small and medium-sized companies – both listed and private – so has really been in the eye of the storm since inflation bedded in, interest rates rose, and we had the rotation away from growth stocks. The result is it is trading on a 33% discount to NAV today.

But for a longer term investment I think it still has merit. As and when the economic situation starts to improve and/or inflation starts to fall giving space for interest rates to fall too, small, and medium companies could get the boost they have been waiting for. They generally do better coming out of a recession and, with valuations looking attractive today, now could be a good entry point. The team behind it is hugely experienced and has access to a very well-resourced team. The group also has a huge resource to tackle the unique challenges of private equity investing.

2) Scottish Mortgage Investment Trust

This trust was hugely popular for a number of years but was hit hard when the macroeconomic picture changed in 2022. Clearly if you’ve held it for the past 12 months you would’ve been disappointed, but buying an investment trust with a track record like this when it is 50% down and trading at a 22% discount would be worthwhile in the long-term.

There are trends going in its favour. For example, the Nasdaq is up almost 30% this year which shows me that either growth stocks were oversold last year or that we are about to enter a rate cutting environment, which favours growth once again. If you like its style, believe in the stories behind the companies it invests in and would have bought it at its height, why would you not buy it today at bargain prices?

3) TR Property Trust

Commercial property trusts have suffered big declines over the past year. This has been driven almost entirely by higher interest rates. If you can get 4.5% risk free in a Government bond, you need a higher yield on a property investment to compensate you for the extra risk. Worries over recession have also hampered the asset class. Much of this is now already priced in though, and we this could be a great entry point for a long-term investor.

You’re getting great dividend yields and high discounts. Higher inflation is helping rental growth and should support capital values as costs for new buildings rise. TR Property Investment Trust has one of the most experienced managers in the business. This trust is currently trading on a discount of just under 10% and the yield is over 5%.