News

Annuity rates rise: Compare to get 15% more retirement income

Retirees are urged to compare providers as the difference between the best and worst offer can mean thousands of pounds more or less in retirement.

Retirees should never accept the offer made by their existing pension provider for an annuity – a guaranteed income for life – without comparing rates elsewhere, retirement specialist Just Group said.

Its analysis on rates over the last two years revealed that the difference between the best and worst providers can be up to 15% a year extra income.

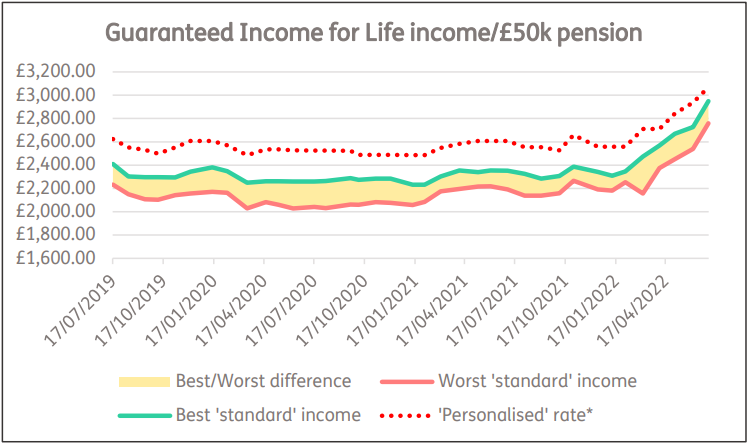

On a £50,000 pension for a 65-year-old, that would mean £206 a month income instead of £180, equal to £7,800 extra income over 25 years.

This is especially important now as annuity rates have risen from their historic lows. Just Group revealed that in January 2022, the worst standard income for a 65-year-old, based on a £50,000 pot came to £2,181, while the best stood at £2,308.

But in July 2022, the worst rate offered was £2,759, while the best offered was £2,949.

Click here to view our Sponsored Content Hub

‘Torpor tax’

Stephen Lowe, group communications director at Just Group, said: “Not shopping around for that extra income – cash that will be paid every month for as long as you live – is like accepting a ‘torpor tax’ that should enrage people who are losing out.”

He added that fully disclosing your medical history and any medication you are receiving plus personal information such as height, weight and alcohol consumption can also make a big difference. Just said for two thirds of retirees, they could get even more by shopping around for personalised rates or an enhanced annuity.

The graph below shows the yellow gap shading between the best and worst rates available to a 65-year-old. The red dots are a guide to the extra income available based on an average of enhanced rates:

Lowe said: “By shopping around – using a professional adviser or broker who takes the retiree’s health and lifestyle into account – they should at least receive the best standard rate and our figures suggest two-thirds will get a rate around the red dotted line.

“The age that is important when considering your income is your biological age rather than your calendar age. By understanding your personal situation rather than assuming you are in good health, pricing can more fairly reflect your situation.”

He added that anyone considering tapping into their private pension money and keen to avoid pitfalls such as paying extra tax or falling victim to scams can get free, impartial and independent guidance from the government-backed Pension Wise service.

“These are complex decisions that may tie you in for the rest of your life, so it is important not to just take the easiest route to get at your money quickly but to make an informed decision you will not regret later,” Lowe said.

Related: See YourMoney.com’s Key points to consider when buying an annuity for more information.