News

Everything you need to know about the pension triple lock

Retirees are braced to receive another bumper state pension pay rise next year due to the triple lock mechanism. We go back to basics to explain what the triple lock is and how it affects you.

The second of three important figures was published today which forms part of a calculation to determine what retirees will receive in state pension payments next year.

It’s all to do with the pension triple lock, and with today’s much-awaited earnings growth figure from the Office for National Statistics (ONS) coming in at 8.5%, it’s likely 12.6 million retirees will see their state pension rise by this 8.5% figure in April 2024.

This was higher than expected, with the ONS noting the NHS and civil service one-off payments made in June and July 2023 following strike action, contributed to the increase from the 8.2% recorded last month.

For some, this could mean an extra £900 in their pockets depending on when they retired.

But why is this? Here’s what you need to know about the pension triple lock and how it impacts retirement income.

Click here to view our Sponsored Content Hub

Pension triple lock explained

The pension triple lock is a mechanism by which the state pension is uplifted for the millions of people in retirement.

It guarantees that the state pension rises each year by the highest of:

- Average earnings growth between May and July (total pay including bonuses)

- Consumer Prices Index (CPI) measure of inflation in the year to September, published in October by the ONS

- Or 2.5%

It was announced by the coalition Government (Conservatives and Lib Dems) back in 2010 and originally used the Retail Prices Index (RPI) measure of inflation in April 2011 before switching to CPI instead for the April 2012/13 tax year.

The reason behind it was to ensure that pensioners, particularly those who relied on the state pension as their only source of income could afford the cost of living and keep pace with inflation and rising wages. Pension poverty statistics helped put this on the map too as the Government looked to reduce the number of older and vulnerable people living in poverty.

It applies to both the basic state pension for those who retired pre-April 2016, and those on the new, flat rate state pension who retired post-April 2016.

How much is the state pension worth and what does the triple lock add?

Currently those who retired pre-April 2016 and who are in receipt of the basic state pension get £8,122.40 a year (£156.20 a week). From April 2024, this figure could rise to £8,814 (£169.50 a week) which is nearly £700 more.

For those who retired after April 2016, the current state pension is £10,600.20 but this could rise £900 to £11,502.40 (£221.20 per week, up from £203.85 a week).

According to calculations by Interactive Investor, the state pension has risen £3,158 in real terms since 2011 when the triple lock was introduced, but it is still one of the lowest in Europe.

Last April in 2022, retirees received a blockbuster 10.1%, meaning they’ve received a combined increase of almost 20% over two years, while workers have seen a 14.5% increase over two years, according to Aegon.

Will retirees definitely see an 8.5% state pension rise in April 2024?

We know two of the three pension lock equations (the standalone 2.5% and 8.5% earnings growth) but there is still one missing piece of the pension puzzle, and that’s inflation.

The latest inflation figure came in at 6.8% in the year to July which is lower than the wage growth figure of 8.5%.

Inflation has also been slowing and is down from the 40-year high figure of 11.1% in October 2022.

The Government and the Bank of England both forecast inflation to fall to 5% by year end, so it seems likely that the earnings growth figure (rather than inflation) will determine next year’s state pension rise.

However, we need to wait until the official September inflation reading is released in October to have all three readings to say for certain that the state pension will rise by 8.5%.

But with the rising wage figure and an uptick in petrol prices, experts suggest inflation could rise at the next publication.

Steve Webb, former pensions minister, and partner at consultancy Lane, Clark and Peacock, said: “Even if inflation were to rise slightly by the time of the September figure published in October, it would probably still be lower than the earnings growth figure.”

Jason Hollands, managing director at wealth management firm Evelyn Partners, said: “Such strong wage growth could impair the retreat of inflation in the coming months. The consumer prices index for August is due next week, and there is speculation that it – and September’s reading next month, which is the final cog in the triple lock – could reveal a plateau or even a tick back up in the rate. The Bank of England has warned that the pace of wage growth is a threat to its longer-term inflation target of 2%, with the implication that continued high pay growth could keep rates higher for longer – in turn raising the risk on an economic slowdown.”

Pension triple lock and the Conservative party manifesto

The other question mark over the pension triple lock is whether the government will commit to it for April 2024.

When retirees were braced to receive the 10.1% state pension rise this April, there was outcry from those on low income or receiving benefits who were also struggling with the cost-of-living crisis but had a real terms cut to pay because of soaring inflation.

Last month, Prime Minister Rishi Sunak confirmed the Government will stick to its triple lock pledge next year. However, he declined to comment last weekend about what would feature in the Conservative party’s manifesto as election campaigning is likely to kick off soon.

It was also Sunak as a previous Chancellor who broke the 2019 Conservative party manifesto by scrapping the triple lock in April 2022 due to distortions created by the pandemic which would have seen retirees receive big increases in their retirement income.

Further, the cost to the Government in maintaining the triple lock is also under the spotlight.

Webb said: “As a rough guide, each 1% on the basic / new state pension costs around £1bn in pension payouts, so today’s figure means the Chancellor will have to find roughly an extra £2.3bn to keep his triple lock promise.”

The high cost of the triple lock

According to the Institute for Fiscal Studies, since the triple lock’s introduction in 2011, the Government has now spent £11bn per year more on the state pension than if it had used a single lock.

Further, maintaining the triple lock could push additional state pension spending up by between £5bn and £45bn per year in today’s terms, taking into account the ageing population.

Steven Cameron, pensions director at Aegon, said: “The huge popularity of the triple lock amongst pensioners is balanced by the huge cost of funding it, which is met by the current National Insurance contributions of today’s workers. All parties must find a way to balance the books. One fairer and less unpredictable option would be to move away from a year-on-year comparison of earnings, inflation and 2.5% to one which averages out across say three years.”

Becky O’Connor, director of public affairs at PensionBee, said: “A state pension ‘pay rise’ for pensioners next year will make the triple lock promise more costly than ever and call into question whether this mechanism of guaranteeing increases can continue.

“Scrapping guaranteed income rises for pensioners entirely would be an overdose of medicine for this problem. The intention of the triple lock – to ensure pensioners can afford to live, is noble. But recent extremes in earnings and inflation have exposed flaws in using single, short time periods of data on which to peg rises. On this basis, reforming it, so that volatile data doesn’t result in unaffordable rises at the wrong time, is worth considering.”

However, O’Connor warned that any “knee-jerk, poorly considered reaction” by the Government to deal with the rising state pension bill now risks harming pensioners for decades to come.

“Without increases in line with earnings or inflation, they would be at risk of real income falls in future,” she said.

However, despite the cost pressures on the Government, Webb gave several reasons why the Government is likely to stick with the earnings growth figure in line with the ‘triple lock’ policy:

- It was a Conservative manifesto commitment in 2019, and has already been broken once – in April 2022 – when benefits increased by the 3.1% rate of inflation rather than the 8.6% rate of earnings growth; breaking the commitment twice in three years could be “highly politically damaging”.

- With only a relatively small gap between earnings growth and inflation, the savings from breaking the triple lock would be relatively modest compared with the “political challenge”.

- The law states that the state pension must rise at least in line with average earnings; breaking that link would therefore require legislation and the government might struggle to get such legislation through, especially in the final uprating before an expected Autumn 2024 General Election.

- Older voters are most likely to turn out to vote, and at present they have the highest likelihood of voting Conservative of any age group; with Conservative support already at a relatively low level, “a policy seen as hostile to older voters could further undermine that support”.

- The earnings growth figure remains higher than the September inflation figure which is published in October.

Indeed, the Government and the Bank of England both forecast inflation to fall to 5% by year end, so it seems likely that the earnings growth figure (rather than inflation) will determine next year’s state pension rise (8.5%)

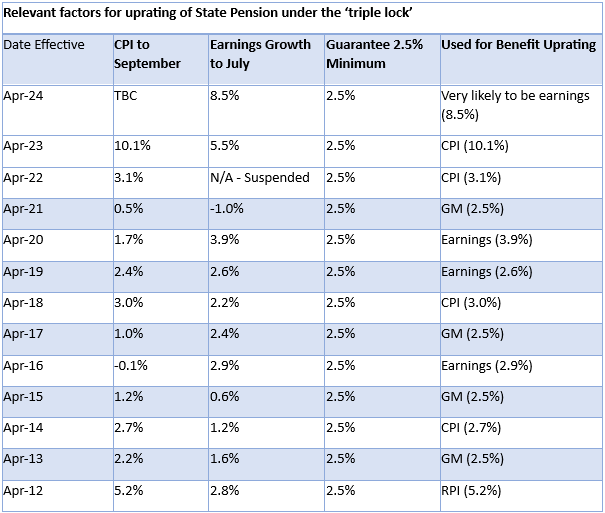

How has the state pension risen over the years and what determined the rise?

The table below shows the level of the state pension and whether the 2.5%, earnings growth or inflation were the determining factor for the rise: