News

Grab a savings deal now as rates rise for the ninth month in a row

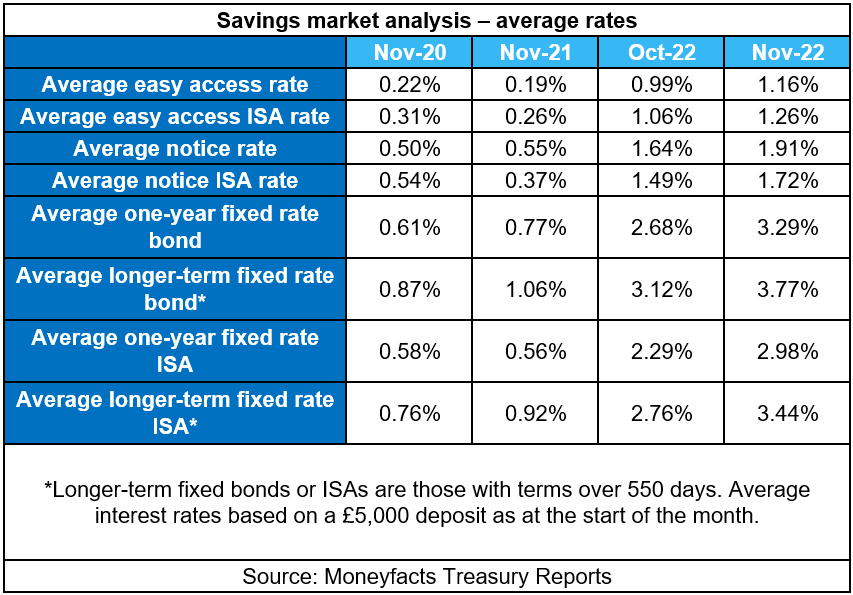

Average savings rates have risen across the board for nine consecutive months, a first for the research site which has been tracking these figures since 2007.

The average easy access savings rate has breached 1% for the first time in a decade, coming in at 1.16%, according to Moneyfacts.

For savers looking to earn a bit more interest on their cash by locking it away for a period, these deals have breached 3% for the first time since 2009.

Savers can now get an average 3.29% on a one-year bond, while the rates on longer-term fixes have risen to 3.77% – the highest point since 2010, Moneyfacts said.

However, it noted that the average shelf life of fixed rate bonds fell by eight days month-on-month to 26 days for November. This is the lowest number of days since March 2009.

And product choice overall fell for the second consecutive month to 1,735 savings deals (including ISAs).

Click here to view our Sponsored Content Hub

ISAs look nicer as rates spike

Average ISA rates are on the rise, with easy access rates now at 1.26%, their highest point since 2013. Average notice ISAs have risen to 1.72%, climbing to a nine-year high.

Meanwhile, the average one-year fixed ISA stands at 2.98%, now at its highest point since May 2012 (3.02%). The average longer-term fixed ISA rate rose to 3.44%, breaching 3% for the first time since October 2012 (3.15%) and now stands at its highest point since June 2012 (3.47%).

Challenger boost savings rates

Rachel Springall, finance expert at Moneyfacts, said these figures are proof of the positive direction of the cash savings market, with further rises expected due to the Bank of England base rate rises.

Springall said challenger brands have continued to be a “notable catalyst for fuelling the fixed bond market” but considering consecutive rises in interest rates, whether savers are prepared to lock away their cash for longer than a year is “debatable”.

“The market may then continue to see volatility for shorter-term bonds and the shelf life of fixed bonds in the months to come,” she said.

Turning to ISAs, Springall said there are “encouraging signs for savers” who wish to use their ISA allowance, especially those with larger pots who may be edging closer to their Personal Savings Allowance (PSA) limit due to rising interest rates.

“However, it remains the case that the rate gap between fixed ISAs and bonds is obvious, so savers will need to weigh up any tax-free allowance they have before they commit”.

Springall added: “As the cost-of-living crisis continues, having quick access to cash could be invaluable and accounts such as an easy access account can offer that flexibility. According to the Bank of England, there was an inflow of just over £3bn into interest-bearing sight deposits [money that can be drawn on demand without penalty] in September, showing consumers are still putting money away into flexible accounts, but there was also an inflow of £3.3bn into time deposits – a sign of consumers taking advantage of the significant rises to fixed rates in recent months. As the savings market remains volatile, consumers and providers will need to act swiftly to keep on top of any prominent offers.”