Blog

BLOG: Vanguard on how to help fund university costs

With changes to the student loan system starting this academic year, we take a look at how to save for university costs and the arguments for and against doing so.

For many parents, university is an important aspiration for their children.

But as with so much in life, there are increasing questions around how you fund a degree. Tuition fees now set an undergraduate back by £9,250 a year, with living costs added on top.

While graduates will not necessarily repay their student loan, and only have to make payments when their income is above a certain level, the idea of accumulating debt so early on is understandably unappealing.

So, how much might you need to save for university? We take a look at the costs below, and some key considerations if your children are thinking about higher education.

How much does a university education cost?

Tuition fees quickly mount up for undergraduates, with a typical three-year degree costing upwards of £27,750. Interest accumulates from the day the loan is taken out, meaning many people are already £30,000 in debt by the time they have taken their final exam.

If you apply for a maintenance loan to cover your living costs, the debt can run up even higher. A student living away from home at a non-London university can borrow up to £9,978 a year, equating to £29,934 over the course of degree.

All in, a graduate who takes out the maximum for both tuition and maintenance loans outside of London can expect to end up around £57,000 in debt.

On the plus side, they may not have to repay all of that. For the academic year 2023/24, graduates pay 9% of their earnings above £25,000 back in student loans, with the debt wiped after 40 years. According to the UK government’s forecasts, that still means that 39% of students starting in 2023/24 will not repay their loan in full.

How can you save for university?

Despite the possibility of not having to repay a student loan in full, many parents have an instinctive reaction against their children taking on so much debt so early in life.

Many therefore look to set aside money ahead of time, potentially with the help of other family members such as grandparents. Junior ISAs (JISAs) are ideal in this respect, offering a tax-efficient way to invest up to £9,000 for the 2023/24 tax year.

While anyone can put money in, only the parents or legal guardians of a child can open one.

The downside to a Junior ISA is that the assets legally belong to the child. That means they can choose to spend the JISA assets on whatever they like once they turn 18.

An alternative option is to use a parent’s tax-efficient allowances when investing, such as an ISA, though there is no guarantee then for grandparents or other contributors that the assets will go towards university costs.

How much could you build up in a Junior ISA?

A Junior ISA could theoretically fund university quite easily if you were able to invest the maximum amount each year. Setting aside £9,000 as cash would add up to £162,000 after 18 years, for example, even without taking investment returns into account.

Few people will be able to invest that amount each year though, particularly if they have more than one child.

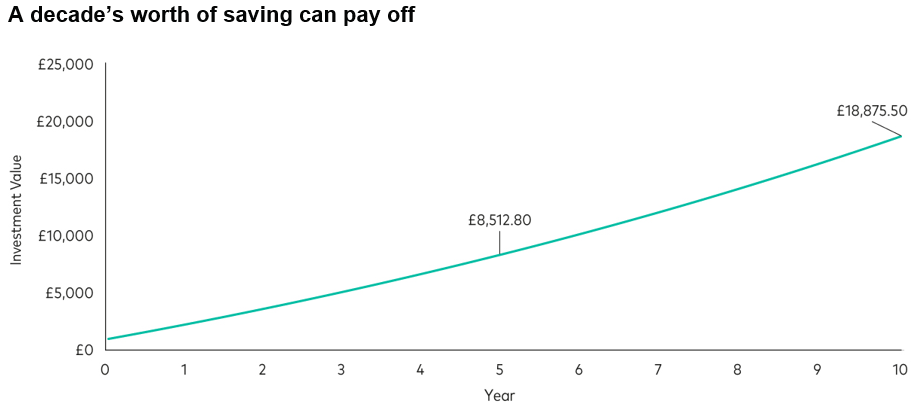

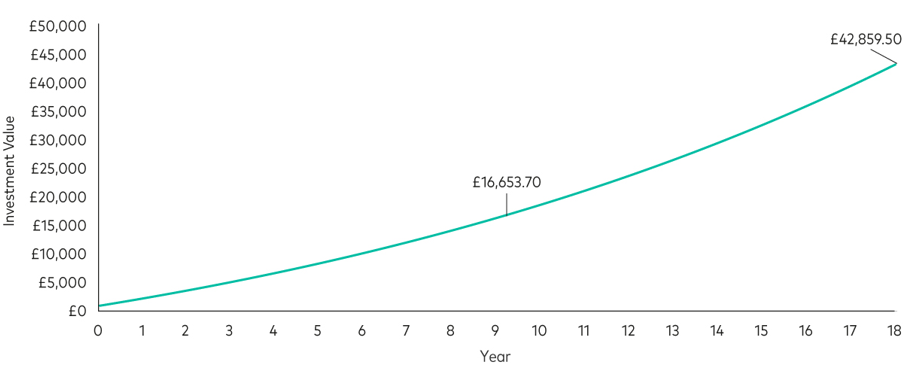

Our chart below shows a potentially more realistic example, where someone starts with an initial £1,000 investment and then saves £100 a month for 10 years. We’ve assumed investment growth of 5.5% per annum after fund and platform costs, compounded monthly (where the interest for month 1 is included in the return calculation for month 2), with the monthly savings rate increasing by 2% a year to take account of inflation.

By the end of the 10 years, our hypothetical investment has grown to £19,000. If you’re really organised, you could start saving from birth. Using the same assumptions as above, but with an investment time period of 18 years, a pot for university savings could amount to just shy of £43,000.

Either scenario could make a big difference to someone’s university experience, helping to fund tuition costs or, in the case of the larger savings pots, funding tuition and helping with living expenses over three years.

Living costs are especially important to consider if an undergraduate is not eligible for the full maintenance loan. The full amount of maintenance loan is only available to those with a household income of £25,000 or less. For those undergraduates who come from a household with an income above £50,000, they are only entitled to a maximum of £6,412 for 2023/24.

Alternatively, any savings could be used towards a house deposit after graduating, giving more time for the investments to grow.

So, should I save for university costs?

Ultimately, there are a lot of different factors to consider when saving for university.

Because student loans are written off after 40 years, there is no guarantee that a student will be better off not taking out a loan (or vice versa).

But having a pool of savings will help to give someone flexibility, whether that’s enabling them to concentrate on their studies and not take a part-time job, or perhaps allowing them to pursue a postgraduate degree or further professional studies, or a completely different goal.

James Norton is head of financial planners, Vanguard, Europe