News

Savings rate rises: The calculations showing the effect of ‘waiting for a better deal’

Savings rates are rising at pace but if you’re sitting on the fence and waiting to see if a better deal comes along before fixing your cash, these scenarios and calculations may help.

From easy access, to bonds, to ISA, savings rates have been on the rise since the start of the year.

And in the last few weeks they’ve really ramped up.

Currently, savers can get the following rates on easy access and fixed savings products, according to Savings Champion data:

- 2.35% on an easy access account (expected profit rate)

- 4.31% on a one-year bond

- 4.62% on a two-year bond

- 4.75% on a three-year bond

- 4.58% on a four-year bond

- 4.61% on a five-year bond.

Savers may be surprised to see that the three-year bond (4.75%), pays more than the best buy four-year or even five-year fixed rate deal.

Anna Bowes, co-founder of Savings Champion, explained: “This indicates the markets are expecting the base rate to rise further in the shorter term, but not over the longer term”.

Indeed, interest rates are forecast to reach 6% next year, according to market consensus.

Effect of a ‘wait and see’

With the expectation that rates will rise in the short term but not for the longer term, what does this mean for you if you’re considering depositing money in a fixed rate savings account?

Bowes said that for savers who are on the fence and leave their cash in a zero interest current account, rates will need to rise “quite significantly” in order to make up the lost interest.

Savings Champion calculations reveal that £10,000 deposited into the one-year bond paying the top rate of 4.31% interest would see savers earn £431 over 12 months.

But, if you leave your cash in a current account paying nothing for one month, you are missing out on £35.92 in interest (£431 divided by 12 months).

Therefore, waiting one month would mean you would need to earn £466.92 in interest to make up the time and interest rate lag (the £431 plus £35.92) which is the equivalent to earning 4.67%.

For those who wait two months, the loss of interest is starker as you would miss out on £71.84 in interest (based on £35.92 each month).

This means waiting two months would require the saver to lock in at a rate equivalent to 5.03% to earn £502.84.

Bowes caveats this by saying: “Of course, if the money is in a best buy access account [earning interest], the rate needed down the line won’t be quite as much.”

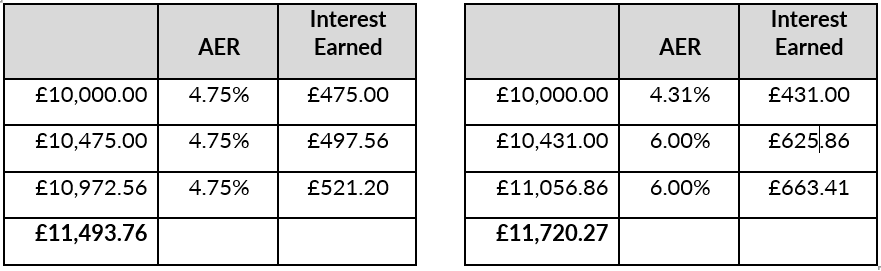

Fixing for three years

Based on the top-paying three-year fixed rate bond (4.75%), savers depositing £10,000 would see a return of £11,483.76, assuming compound interest.

Bowes explained that if instead savers put the money in a best buy one-year deal paying 4.31% and in a year’s time the best two year is paying 6%, then savers will earn more interest over the three-year period.

However, if the rates fall or remain the same, savers will lose out.

The table below highlights these calculations:

Bowes said: “The difficultly of guessing what will happen is that often bond rates have already priced in market expectations of further base rate rises.”

She added that very few bonds allow early access “so you really do need to be confident that you can tie up your money for the term, before you commit”.