News

Warning as more people could pay tax on savings for the first time

The successive base rate hikes could push more Brits into paying tax on their savings interest for the first time since the introduction of the Personal Savings Allowance. Here’s what you need to know.

- £35k in top one-year fixed rate bond could see you breach the £1,000 Personal Savings Allowance

- Last year, basic rate taxpayers required £91k to go over the Personal Savings Allowance threshold

- Basic rate taxpayers paid £132m in tax on savings in 2021/22 but will jump to £332m in 2022/23

- Higher rate taxpayers paid £380m in 2021/22 but will soar to £983m in 2022/23

- How to shelter your savings from tax

- What to do if you breach your Personal Savings Allowance

- Will the Personal Savings Allowance thresholds rise amid base rate hikes?

There have been six consecutive base rate hikes by the Bank of England since December 2021, which have resulted in savings rates on cash accounts also rising at pace.

While this is good news for savers who built up cash buffers amid the pandemic (though many may be drawing on these reserves amid the cost-of-living crisis), it now also means many more people may be closer than ever in breaching the Personal Savings Allowance (PSA) for the first time.

The PSA was introduced in April 2016 and means any savings earned in banks, building societies, peer-to-peer lending, government or company bonds and credit unions won’t be taxed up to a certain limit based on the current income tax you pay.

Basic rate taxpayers can earn £1,000 in savings interest tax-free each tax year, while higher rate taxpayers can earn £500. Additional rate taxpayers don’t receive a PSA. If you have a joint account, interest will be split equally between the account holders.

The PSA aimed to reduce the amount of tax people pay on their savings income, and the government claimed it would take 95% of taxpayers out of paying any tax at all on their savings income. See YourMoney.com’s Personal Savings Allowance guide for more information.

Click here to view our Sponsored Content Hub

However, in the last few months, savings rates have climbed, and they’ve not been this high since the introduction of the PSA six years ago.

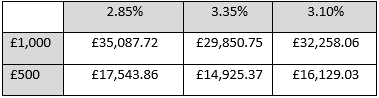

Calculations by Savings Champion reveal basic rate taxpayers would need to save just £35,000 in the current top-paying 2.85% one-year fixed rate bond to breach the £1,000 PSA. Meanwhile higher rate taxpayers would need to deposit just £17,500 to go over the threshold.

A year ago, the top paying one-year bond offered savers 1.10%. This meant a basic rate taxpayer would overshoot their PSA of £1,000 only with a hefty deposit of £91,000 – nearly three times as much in holdings compared to now.

And given today’s latest base rate hike, if lenders were to pass on the full 0.5% increase to customers in the form of higher savings rates, a top one-year savings account paying 3.35% would allow a basic rate taxpayer to save just under £30,000 before breaching their respective PSA, while a higher rate taxpayer would be on the edge with just under £15,000.

If a more modest 0.25% increase was applied – as lenders don’t always pass on the full Bank of England base rate rises and much of this has already been priced in by the markets – it would mean £32,000 and £16,000 in savings for the differing taxpayers respectively.

Source: Savings Champion

Anna Bowes, co-founder of Savings Champion, says: “When the PSA was introduced in April 2016, the highest paying one-year bond was 1.91% rising to a high of 2.15% in August 2018 before falling to as low as 0.58% in March 2021. Savings rates are at their highest since the PSA was introduced.

“What matters here is on what date the interest is paid. If you open an account today and choose for the interest to be paid/added annually then it will count in the 2023/24 tax year. Whereas if you have the income paid/added monthly, it will start to count now too.

“However, paying 20% or 40% on your savings interest is better than earning nothing with a bank.”

‘Savers risk sleepwalking into a tax bill’

Shaun Moore, tax and financial planning expert at Quilter, says as the base rate continues to move upwards, breaching the PSA will become more of an issue for savers.

He says: “For some time now, many savers will not have been concerned with paying tax on interest as the rates were so low. Since 2016, most interest has been paid gross with any personal tax being paid via self-assessment.

“People now need greater awareness of the PSA or they risk sleepwalking into a tax bill.”

James Blower, founder of The Savings Guru says savers have been told for years that ISAs (tax-free savings accounts) weren’t worth bothering with because of the introduction of the PSA.

“The advice to savers needs to change. Money is flooding out of ISAs, and has been doing so for the last year, with £1bn out in June alone.

“£35,000 for basic rate taxpayers and just £17,500 for higher rate taxpayers on the top one-year bond (2.85% from OakNorth) is enough to trip over the PSA. This is becoming much more of an issue for savers, and I don’t think many are aware that it is.

“Some won’t appreciate how much rates have gone up this year (more than doubled in many product categories) and will get hit when they come to do their tax return and realise they are over the PSA limit.”

He adds that the good news for savers is that easy access ISA rates are also increasing, with the best “almost on par with their ordinary counterparts”.

“Newcastle Building Society pays 1.5% on easy access ISAs and I’d suggest savers over the limit look to use that for easy access savings and use ordinary fixed rate bonds for their PSA as, for example, the best one-year fixed rate bond (OakNorth) beats the best one-year fixed ISA (2.25% Kent Reliance) by some distance”, he says.

And he echoes Bowes’ point that it is still much better to pay the tax than it is to leave savings in a paltry interest earning account.

Blower says: “Not just because you’ll earn more money but, until more people start switching from the big banks, they have no incentive to improve rates which are still as low as 0.1% in far too many cases, despite six consecutive base rate rises.”

Personal Savings Allowance ‘does have drawbacks’

Will Davies, chief deposits officer at Ford Money, says: “PSAs have been widely praised since their introduction in 2016 for relieving so many people of the tax burden on their savings and simplifying the application process.

“However, PSAs do have drawbacks, one of which is that the amount has not changed in six years. As the country faces economic pressure, interest rates continue to rise, which is great news, but an increasing number of people will face an additional tax burden as they reach tax allowance thresholds.

“If this problem is to be solved, the government’s best option would be to raise the PSA, which would remove many people from taxable savings and encourage more savings activity. However, it is not all doom and gloom, many banks and online financial providers offer a variety of tax-efficient ISAs that shield customers from paying tax (on amounts up to £20,000 per year). If a person wants to avoid exceeding their PSA for the tax year, they should consider shopping around and opening an ISA if they haven’t already.”

For Moore, savers who look beyond ISAs should “limit exposing savings to interest paying securities”.

He says: “Shares can also be used to makes use of the £2,000 dividend allowance. Investment bonds, particularly for higher or additional rate taxpayers, can also shield income from personal taxation by deferring it until your income falls – perhaps in retirement.

“It is also crucial to plan as a couple as each partner has an allowance – personal, starting rate for savings, PSA and dividend allowance – and you should plan together to use them most effectively.”

Statistics from HMRC revealed there were 8.02 million people benefitting from the PSA in 2019/20 at a cost to the exchequer of £310m, 8.16 million people were benefitting from the PSA in 2020/21 at a cost of £300m and 8.33 million in 2021/22 at a cost of £220m.

While the number of people benefitting from the PSA has been steadily rising, the income tax liability on savings has been in decline.

In 2019/20, basic rate taxpayers paid £170m income tax on savings while in 2020/21, this figure came in at £145m. In 2021/22, it stood at £132m. This figure has been in decline over the last three tax years, but HMRC estimates for 2022/23 suggest the income tax on savings will jump to £332m – £200m more in just a year.

For higher rate taxpayers, £474m was paid in 2019/20, £404m in 2020/21 and £380m in 2021/22. Again this figure is set to soar to £983m – £600m more in just a year.

However, there are signs that cash savings are in decline. Latest Bank of England Money & Credit statistics revealed the combined net flow into both deposits and NS&I accounts in June was £1.9bn, down from £5.6bn in May and below the average monthly net flow of £4.7bn during the 12-month pre-pandemic period up to February 2020.

What to do if you go over your Personal Savings Allowance

Before the PSA, banks and building societies deducted income tax from interest earned on products and accounts – apart from ISAs – at a flat rate of 20%, the basic rate of income tax.

For higher earners, the additional 20% was either collected through PAYE codes or via tax returns.

Following the introduction of the PSA, the flat rate is no longer deducted, with providers required to report savings information to HMRC as it places more reliance on PAYE codes.

For those who go over the PSA, you’ll pay tax at your marginal rate on amounts above £1,000 or £500. For those who are employed or get a pension, HMRC will change your tax code so you pay the tax automatically. To decide your tax code, HMRC will estimate how much interest you’ll get in the current year by looking at how much you got the previous year.

However, as this may not have been an issue for people last tax year, YourMoney.com asked HMRC if savers should submit tax returns or contact HMRC with more up-to-date savings interest information. It said employed people should contact HMRC to report savings interest that’s over the threshold for the first time.

If you usually complete a tax return, you should report any interest earned on savings there as normal.

If you’re not employed, aren’t in receipt of a pension, and don’t usually submit a self-assessment tax return, your bank or building society will tell HMRC how much interest you received at the end of the year. HMRC will tell you if you need to pay tax and how to pay it.

Blower says: “Banks are still reporting interest paid to HMRC, so you may well get contacted by them to do a return but the responsibility is on the individual now.

“The PSA was bought in to reduce admin for HMRC. Under the old system you paid tax automatically and then had to claim it back or get exemption (non-taxpayers) or pay more (higher rate taxpayers).”

He adds that as the PSA is unchanged since its introduction, and with rising rates, “it may be HMRC pushes for higher allowances if the admin burden increases with rising rates”.

“What it [HMRC] won’t want is all those people who were only doing tax returns because of interest on savings, having to start doing them again,” Blower says.

Moore adds: “Given the pressures on cost of living, there is a case that the government should increase the PSA. It has been static since 2016 and with inflation sky high, an adjustment to limit would offer a welcome helping hand to the UK’s hard-earned savings.”

‘Savings tax kept under review’

Asked whether the government would consider changing the PSA thresholds in light of the cash buffers built up over the Covid pandemic and amid rising interest rates, a treasury spokesperson, said: “The government considers that the UK has a generous savings tax regime that compares favourably to other countries.

“In addition to the PSA, individuals may also save up to £20,000 per year in an ISA and earn from tax-free returns, and benefit from the Starting Rate for Savings on up to £5,000 of savings income.

“The government keeps all aspects of savings tax under review, with any changes announced at a fiscal event in the usual way.”