Today (October 12) marks National Savings Day, an annual event created by US financial services group Capital One to help investors think about their saving (and spending) habits and what they can do to improve them if they’re not saving enough for their future needs.

Saving money also helps you reach your financial goals. This can vary from short-term goals, such as buying a new phone or pair of shoes to long-term goals, like retirement, buying a new home or helping your children with university fees.

Research from the Institute for Fiscal Studies show just how concerning the savings gap is for the UK. It found that 61% of the middle-earning private sector employees who are contributing to a pension are saving less than 8% of their earnings, and 87% are saving less than 15% – the level Lord Turner’s Pension Commission thought was necessary.

The Bank of England backdrop – good news and bad news for savers

The Bank of England has been hiking rates for months in a desperate bid to get soaring inflation under control.

In fact, there were 14 consecutive increases in the base rate from December 2021 to cool spending and get inflation closer to its 2% target. At its last monthly meeting in September, the Bank’s Monetary Policy Committee narrowly voted in favour of keeping rates at 5.25%.

The good news for savers is that banks have been passing on some of these increases, which means their money is earning more in their savings accounts.

But, we must remember that inflation erodes any potential savings to a degree. Say you put your money in a bank account that pays you interest at 4%. A year later you’ll have 4% more money. But what if inflation is more than 4% (it is currently 6.7% in the UK). This would mean that although you’ve got more money, it can purchase less than the amount you began with.

Freeing up cash

It’s also worth exploring whether you can cut your outgoings and free up some money that can be tucked away. If you could find just £10 a month that would give you an extra £120 in a year. Investing that could see it grow further.

So, how much should you be saving? Well, one approach is the 50-30-20 rule. This suggests that 50% of your income should go on essentials, 30% on non-essentials, and 20% into savings.

Investing

How much money you’ll need in the future is very much an open-ended question and will depend on your individual goals, aspirations, and existing savings.

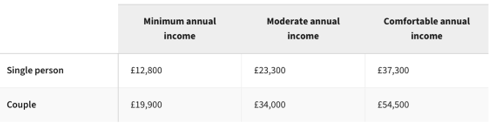

For example, The Pensions and Lifetime Savings Association publishes annual estimates for ‘retirement livings standards’ at three levels of income: ‘minimum,’ ‘moderate,’ and ‘comfortable.’ Estimates for 2023 found that a single retiree would need a minimum annual income of £12,800, this rises to £23,300 and £37,300 for the moderate and comfortable retirement lifestyle. These numbers are higher for couples in retirement.

The average life expectancy for 65-year-olds in the UK is 86 for women and 84 for men. If we say an average person lives 20 years in retirement, to do so comfortably (one that allows you to have a couple of holidays each year and to be a ‘little spontaneous’ with your money) they would need a total of £746,000. We should note that those with a full state pension are entitled to £203.85 a week, this kicks in one you are 66-years of age, so that would take away some of the burden.

Ultimately, data from the Department for Work and Pensions shows almost nine in 10 (89%) of the working population are not on track to meet the PLSA’s definition of a ‘comfortable’ retirement.

Active funds to fill the void

With bonds yielding attractive returns once more, I’d look to the likes of a strategic bond fund like Aegon Strategic Bond or the Jupiter Strategic Bond. Both can invest across all types of bonds and – in addition to the attractive yield (both offer more than 5%) – may also deliver capital growth.

Presuming your investment would need to last two decades, an element of growth will be essential. For this, I’d look to global equities with a fund like T. Rowe Price Global Focused Growth Equity, which has returned almost 75% to investors in the past five years. Those preferring to stay closer to home might consider the likes of JOHCM UK Dynamic, a 30-50 stock portfolio of companies of all-sizes within the UK market.

If you’re looking for something a little different, then two areas with excellent long-term growth potential would be India and biotechnology, where I’d consider the likes of the Goldman Sachs India Equity Portfolio and AXA Framlington Biotech respectively. Both are not for the faint hearted, but should offer greater returns in the next 10-20 years.

Darius McDermott is managing director of Chelsea Financial Services & FundCalibre