News

Named and shamed: Banking giants’ sub-1% savings interest as challengers pay SIX TIMES more

Loyalty really doesn’t pay as it’s revealed the banking giants are getting away with offering savers less than 1% interest on their cash, while challengers are paying much more.

Banking giants are already under fire and are facing tough questions over their easy access savings rates which are a fraction of the current 4% Bank of England base rate.

But analysis lays bare the paltry rates they offer compared to what’s being paid by challenger banks and mutuals.

According to Moneyfacts Compare, Barclays Bank is paying the lowest rate in its easy access – Everyday Saver – at just 0.55% gross on £10,000. Santander’s Everyday Saver pays a smidgen more at 0.6%, while Lloyds, NatWest and RBS pay 0.65%, with the latter expected to increase this to 1% from 21 March 2023.

Elsewhere, TSB pays 0.7%, Halifax and Bank of Scotland each pay 0.8% and HSBC leads the pack with its 1.19% offered on its Flexible Saver (Standard).

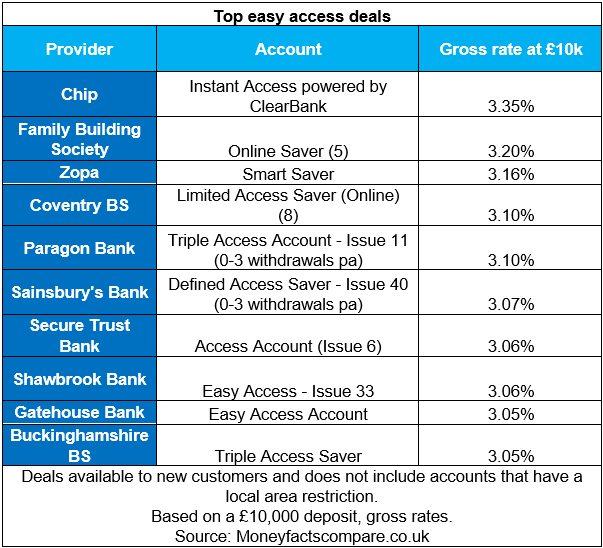

By contrast, these challenger banks are paying up to six times more than their heavyweight competitors:

‘Loyal savers not benefiting’

Rachel Springall, finance expert at Moneyfacts Compare (formerly Moneyfacts), said: “Convenience is costing savers who keep their cash stashed in an easy access account with a big high street bank. As the Bank of England base rate has risen all the way up to 4%, it is evident loyal savers have not seen the full benefits passed on to them.

“The Treasury Committee is seeking answers from various banking giants, including Barclays Bank, HSBC, Lloyds Banking Group and NatWest Group as to why specific easy access accounts pay much less than base rate. It will be interesting to see the responses, which are anticipated this week, particularly when challenger banks and building societies are increasing rates.”

Springall added that for savers who compare the top easy access rates, they will find rates of 3% or more, as she reminds people that “every brand has the same protections in place as the big bank brands do, being covered by the Financial Services Compensation Scheme (FSCS)”.

But she said: “However, every institution can have its own reasons and margins in place that leads it to assess its savings rates. Challenger banks and building societies may well prioritise offering a fair deal compared to the wider market and adjust their rates to cope with demand or other market influences. Mutuals may be worth considering, not just for their savings rates, but also for their principles and the support of local communities and charities. It will be down to savers to compare the rates on offer and move their money, so it is wise to review any accounts often and not presume they will see their rate rise in line with base rate.”

Related: Battle of the app-only providers sees interest rates ramp up

How to get 7% interest without tying up your savings for years